Report to Members: 2025 Letter from the CEO

Listen to the 2025 Letter from the CEO

Read by Martin Leitch

Dear fellow members,

Thank you for your continued trust in PURE. Serving you and stewarding a member-owned organization on your behalf are responsibilities we take seriously and privileges we value deeply.

As we reflect on 2025, our thoughts are first with the members and communities impacted by losses, particularly the devastating California wildfires. To those continuing to recover and rebuild, our hearts are with you.

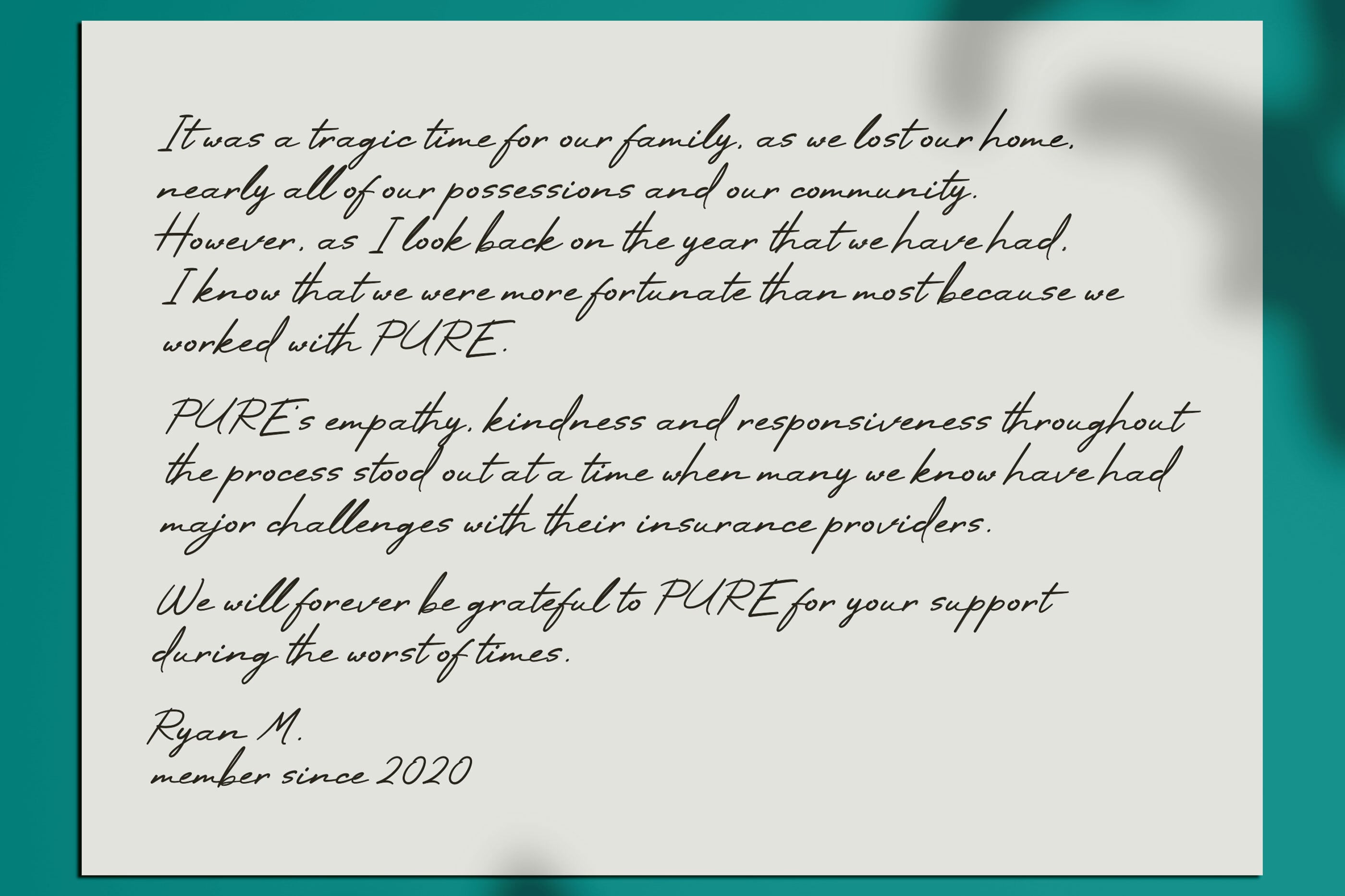

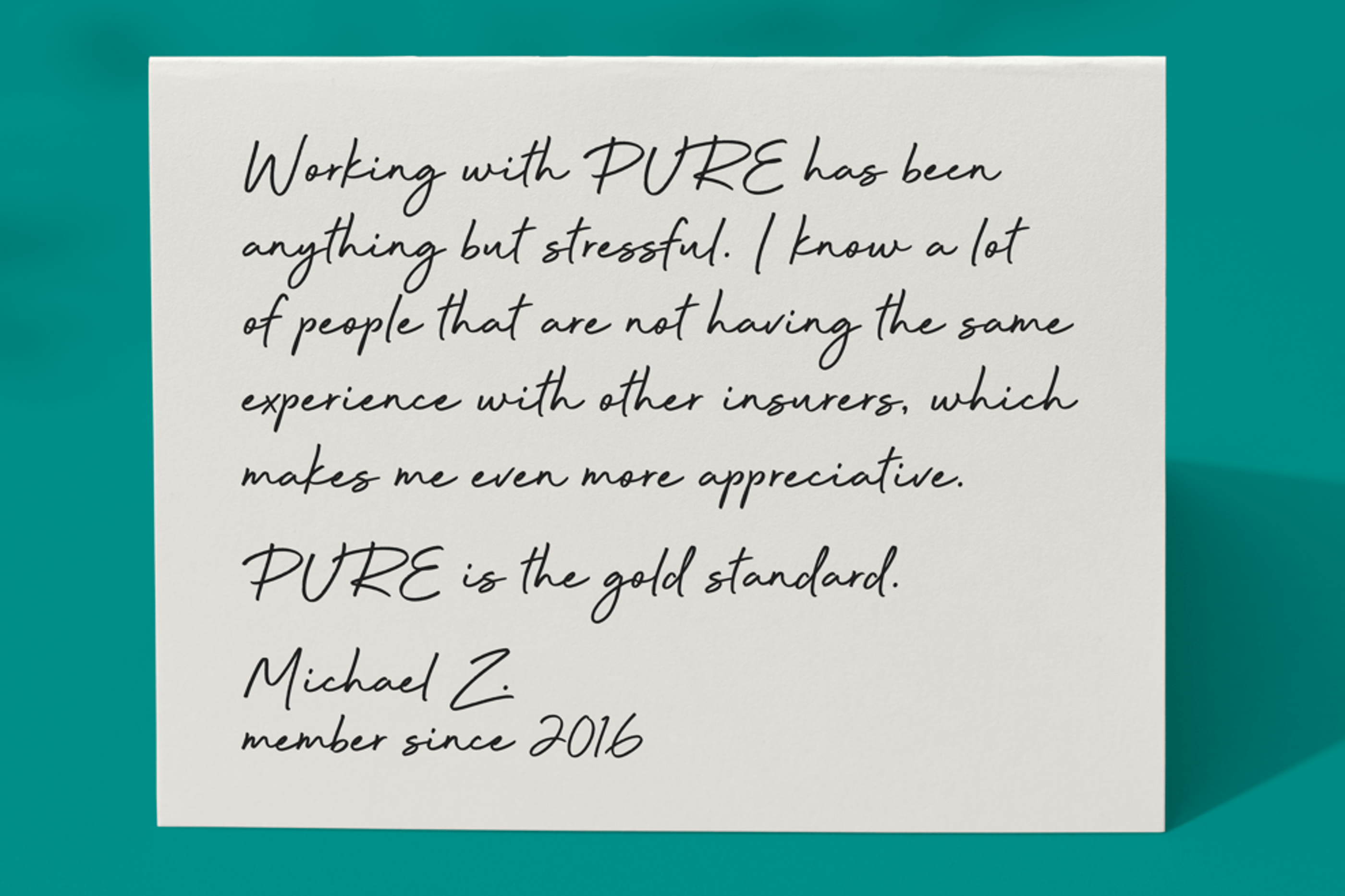

I am immensely proud of our Claims and Service teams, who were trusted to act quickly and do what was right when it mattered most: being available in person, securing temporary housing within days, engaging world-class hygienists and custom builders, and providing quick financial assistance. Their professionalism, judgment and care are defining strengths of PURE.

Read more about PURE's response

I am also proud of our members. More than 30 of you offered access to your unoccupied homes when housing was scarce, extending help to fellow members in need. Moments like these remind us that membership can be so much more than insurance, and why preparedness, compassion and responsiveness matter so deeply.

The many thoughtful notes we received from affected members were so encouraging, and that sentiment is reflected in a 97% claim satisfaction score. I firmly believe there is no better insurance company to have by your side during a traumatic event than PURE.

2025 results

PURE made steady, meaningful progress in 2025. The membership grew to over 120,000 responsible families, supported by an exceptional voluntary retention rate of more than 95%. PURE’s direct written premium grew by more than 15%, pushing total premium under management (including PURE Specialty) to more than $3 billion.

In a year when we responded to the largest catastrophe loss in our history, underwriting results were strong with a net combined ratio of 98.8%. Our recent results reflect disciplined progress towards our goal, which is, over time, to target a net combined ratio of just under 100%, where premiums fully cover losses and expenses, including the cost of reinsurance, with a modest underwriting gain to help build the balance sheet.

120,000+

responsible homeowners now make up our membership

responsible homeowners now make up our membership

96%

voluntary retention rate

voluntary retention rate

$3 billion

total premium under management

total premium under management

98.8%

net combined ratio

net combined ratio

Nearly $170 million

allocated to Subscriber Savings Accounts since PURE's inception

allocated to Subscriber Savings Accounts since PURE's inception

Sharing success through our reciprocal model

Insurance is unique in that the true cost of claims is unknown when a policy is issued. As a result, annual outcomes are inevitably better or worse than expected. When claims costs are low and PURE builds capital, members can share in PURE’s success through allocations to Subscriber Savings Accounts (SSAs).

Following our strong 2025 performance, we have received regulatory approval to allocate $50 million to members’ SSAs this spring. This is PURE’s first SSA allocation since 2020 and brings our total amount allocated since inception to nearly $170 million.

SSAs are perhaps the most tangible benefit of PURE’S unique membership structure and an important point of differentiation against most traditional insurers where investor interests take priority over policyholders.

For members newer to PURE, SSAs are notional accounts held for each active PURE member that reflect their individual share of PURE’s capital. PURE Gold members, those who have been with us for 10 years or more, are eligible for discretionary distributions from these accounts. I’m pleased to announce that 5% of PURE Gold members’ SSA balances (currently valued at $2.6 million) will be returned to them, either through a credit against their outstanding premium balance or a cash payment.

We aim to price fairly, and when results exceed expectations, our structure allows us to share these capital gains with the membership. SSAs are perhaps the most tangible benefit of PURE’s unique membership structure, and an important point of differentiation from most traditional insurers where investor interests too often take priority over policyholders.

A market moving toward stability

The past several years have been challenging across the insurance industry, marked by elevated catastrophe activity, higher reinsurance costs and more severe claims. While these conditions require discipline and difficult decisions, we are beginning to see signs of greater stability across most geographical regions and product lines.

Personal excess liability is a notable exception. Despite being one of our most important coverages, availability and affordability continue to deteriorate in certain states. Industry data from Assured Research shows that insurers representing roughly one-third of the personal excess market are experiencing average annual loss increases of 14%, with underwriting results worsening in recent years. Within PURE’s portfolio, the frequency of very large claims has increased by more than 130%, driving the need for pricing adjustments as the severity of claims becomes more unpredictable.

These pressures are intensified by a less predictable legal environment, where liability theories continue to expand and, even with the same facts, outcomes can vary widely across jurisdictions. We continue to work with the the National Association of Mutual Insurance Companies (NAMIC) to push back against unsustainable liability trends that are driving costs and constraining coverage.

Preventing loss, protecting what matters

Loss prevention sits at the heart of how we serve members. Helping reduce risk—from water damage and electrical fires to wildfire preparedness—means fewer disruptions and safer homes. When losses are prevented or minimized, everyone benefits.

In 2025, we provided loss prevention guidance to the owners of more than 25,000 homes. We also continued to expand pilot programs into more comprehensive loss prevention offerings to stop small problems from becoming major ones. One example is Ting, our first prevention initiative, which is now active in more than 30,000 PURE-insured homes. It detects early warning signs of electrical issues so they can be addressed before sparks, smoke or fire trucks are involved. To date, Ting has helped prevent more than 300 potential electrical fire incidents—many of which could have become serious, costly losses. We cover the cost of the device and the annual subscription because we believe prevention should be easy to adopt and hard to ignore.

Behind the scenes, our Situation Room monitors risks around the clock. Last year, the team reviewed more than 200 alerts each day from hundreds of sources related to wildfires, structure fires, flooding and others. Roughly 5,000 of those alerts prompted proactive outreach to members who may have been in harm’s way. During wildfire events, our response partner, Capstone, deployed fire trucks 19 times across seven states to support members when conditions were most threatening.

Looking ahead, we will continue to invest in tools, insights and services to help members better understand and reduce risk before a loss occurs. One area of focus is proactive home maintenance. We are partnering with two firms to test their effectiveness and gauge member interest. Our goal is simple: help members address issues earlier, more conveniently and with less stress.

Expanding protection against flood risk

Flooding is now the nation’s most costly natural hazard, driven by frequency rather than scale. Extreme rain events are occurring more often, in more places—including areas once considered low-risk. A recent AccuWeather study found that 24-hour rainfall events exceeding four inches have increased by roughly 70% since the mid-1990s, materially expanding flood exposure. A single severe storm can overwhelm drainage systems and cause significant damage, regardless of proximity to rivers or coastlines.

Yet the coverage remains underutilized; among PURE members, fewer than 12% carry any flood insurance. The reality is simple: if it can rain where you live, it can flood.

To better protect the membership, we introduced a private primary flood solution designed to provide an exceptional experience and broad protection, including coverage for basements. In many of the communities we serve, the pricing for this coverage is modest relative to the potential severity of loss and the protection it provides. We strongly encourage every member—regardless of perceived risk—to talk to their broker about flood coverage.

Flood coverage

Among members who do not have flood coverage from PURE or through our NFIP write-your-own program:

More than 13,000 homes are at “moderate” risk of pluvial flooding

More than 13,000 homes are at “moderate” risk of pluvial flooding

More than 800 homes are at “very high” or “extreme” risk

More than 800 homes are at “very high” or “extreme” risk

Pluvial flooding is a nationwide concern and affects even areas considered “low-risk.” In fact, one-third of NFIP flood insurance claims come from outside high-risk areas, and many losses go uninsured, so the true share of affected homes is even higher. If your home has been identified as at risk, we will proactively reach out—in partnership with your broker—to discuss your flood coverage options.

Blending technology with personal service

As PURE continues to evolve, hospitality remains at the heart of how we operate. Whether through a claim, a service interaction or proactive outreach, members should always feel cared for and understood.

Like most companies, we are investing meaningfully in digital capabilities and artificial intelligence to improve efficiency and ultimately reduce costs. The outcomes we seek from these investments, however, may differ from most organizations. “Margin expansion” is not our objective; delivering a better, and even delightful, member experience is.

“'Margin expansion' is not our objective; delivering a better, and even delightful, member experience is.”

We will use new tools to respond faster and more accurately, putting more control in members’ hands, but technology will never replace our people. Members will always have access to a human at PURE. Just as importantly, our investments in technology are paired with investments in our employees through training and development, ensuring they are equipped to deliver exceptional service in a changing environment.

Whether you choose to engage digitally through the PURE mobile app or your online account, or work directly with one of our team members, you can expect the same thoughtful, personal service.

Looking ahead with optimism and gratitude

As we enter 2026—a milestone year marking PURE’s 20th anniversary—we do so with gratitude for the trust, partnership and support we’ve received over the past two decades, and with confidence in what lies ahead. PURE is financially strong, operationally disciplined and aligned with the long-term interests of our members. While the world around us continues to change, our guiding purpose remains constant: We want you to love your insurance.

Thank you for your trust and for being part of the PURE community.

Sincerely,

Martin Leitch

Chief Executive Officer