Report to Members: 2024 Letter from the CEO

Listen to the 2024 Letter from the CEO

Read by Martin Leitch

Dear fellow PURE members,

As I sit down to write this letter in the early days of 2025, my heart aches for our members affected by the Los Angeles wildfires. More than 40 of our fellow members lost their homes and belongings, and many more suffered partial losses as a result of these devastating fires. While we all wish things like this never happened, these unexpected and unwanted events are why PURE exists. We are committed to serving members with care, empathy, transparency and speed in their greatest time of need.

“We are committed to serving members with care, empathy, transparency and speed in their greatest time of need.”

I’m exceptionally proud of my colleagues and our readiness for, and response to, this event. While the fires were still burning, 18 of our highly experienced claims adjusters, including our Chief Claims Officer, Derek Zahn, touched down in Los Angeles, ready to get to work. We inspected all reported losses in an expedited manner and began issuing payments before the fires were out.

This passion to serve was shown throughout the organization. One adjuster drove eight hours round-trip to meet with a couple so he could explain in-person how their coverage would apply; several others dug through the rubble of what used to be members’ homes to recover jewelry and other sentimental items; and yet another saved koi fish from what remained of a member’s pond.

Outside of the Claims team, many other team members worked extended hours monitoring the fires and supporting members—one even voluntarily canvassed the burn area by scooter in the very early days to assess damage because cars could not gain access.

Read about our catastrophe response

Combined, the Palisades and Eaton fires will rank among the top five natural peril-caused insurance losses of this century, and individually, they will rank as #1 and #2 for costliest insured wildfire losses in U.S. history.

While the magnitude of these fires is indisputable, we plan for events like this—so our balance sheet remains strong. That said, this is a timely reminder of what Mother Nature is capable of, especially in catastrophe-prone areas, and that we must continue to smartly manage aggregation and charge premiums that reflect the risk.

Where we go from here

Adapting to new weather patterns and evolving risk will be a collective effort. State and municipal authorities need to ensure adherence to proper building codes and public safety. Insurance regulators need to ensure protections for consumers while also providing insurance companies with a healthy environment in which to operate. Insurance companies need to provide adequate coverage as well as sound and practical risk management advice and solutions. And policyholders need to act on that advice, doing their part to prevent claims.

Explore the rest of the report

Together, we believe we can continue to offer broad coverage at a fair price to our members with properties exposed to a range of natural catastrophes. California, however, has been a challenging insurance market since long before the Los Angeles wildfires, which now put the availability and affordability of homeowners insurance at that much greater risk. I hope this event triggers the positive changes necessary to maintain an efficient insurance market in California, but significant adjustments are required for this to become reality. PURE is ready and willing to work with all relevant stakeholders.

Reflecting on 2024

We have been on a journey to improve the profitability of your insurance company these past few years, and 2024 reflected the impact of these challenging efforts with a significant improvement in results.

While overall public sentiment towards insurance companies has been negative, with concerns over misalignment and rising costs, I hope you have peace of mind in knowing that our member-owned reciprocal structure means we are acting in the best interests of the membership. We will continue working hard to earn and keep your trust.

While PURE has not been exempt from the challenge of rising claims costs, which contributed to premium increases over the past several years, our reciprocal structure allows us to deliver exceptional coverage and service while rewarding the most responsible members with lower premiums over the long run.

To that end, my colleagues and I are reaffirming our commitments to the membership. These serve as guideposts and set aspirational standards to which we hold ourselves accountable—and you should too.

Our commitments to you

#1: We will make your experience easy and delightful.

We’ll approach every interaction with care, humanity and warmth. During Hurricanes Helene and Milton, over 200 PURE employees from across the organization made pre- and post-storm outreach calls to nearly 4,000 members in impacted areas. Our priority was to make sure our members were safe and to provide assurance and simple human connection in an unnerving situation. We take pride in the fact that we were the first insurance company on the ground in certain areas, bringing with us a network of water remediation and tree removal services to start repairs as quickly as possible.

In 2024, we responded to over 33,000 claims and received an industry-leading CSAT (claims satisfaction score) of 91%. This is your insurance company, and our most important goal is to promptly and efficiently restore you after a loss.

#2: We will play an active role in loss prevention.

The best claims experience—no matter how good our service is—is the claim that never happens. By working together, we can make progress in reducing the occurrence of preventable claims, which is the first step in making sure premiums remain fair and reasonable—something I know many of you are keen to see, but something we cannot do without your help.

Interior water damage continues to be the most common cause of loss among the membership, and we are working very hard to break this trend. Throughout 2024, we tested many new devices and services designed to prevent these claims, and we are excited to pilot several of them in 2025.

#3: We will be highly selective about who we let into the membership.

We reserve membership for the most responsible homeowners, which helps keep claims costs down and, in turn, allows for lower premiums. In 2024, we welcomed nearly 9,500 new responsible members to PURE in the U.S. and following our launch in Ontario in late 2024, we’ve begun welcoming new members in Canada.

As mentioned earlier, we strive to be a permanent home for responsible members. Our voluntary member retention during the year was just shy of 96%. Through continuous improvement, our goal is to get this number closer to 100%.

#4: We will charge a fair price.

Unlike traditional stock insurance companies, maximizing underwriting profit is not a goal at PURE given our reciprocal structure. Instead, our long-term goal is to charge the “right” price—essentially, to break even over time (after calculating premiums collected minus claims costs, expenses and the cost of reinsurance). I’m pleased to share that we met that break-even goal in 2024 and produced a net combined ratio of 100%. Based on the favorable underlying trends we are seeing, we have started the process to moderate future rate increases for most homeowners.

#5: We will be solutions-focused.

As risks continue to evolve, we’ll create new and enhanced products to address our members’ most common needs, including enhanced flood protection, which you can learn more about from a Q&A with our Chief Underwriting Officer.

I hope reading these commitments furthers the trust you have in us and in our dedication to serving you and your family. I can confidently say our enthusiasm and excitement to serve the membership has never been stronger.

Through every interaction, we strive to create a member experience so compelling you never want to leave. We want you to Love Your Insurance. Most people don’t think of insurance as something to love. But we believe that when done right, it can be.

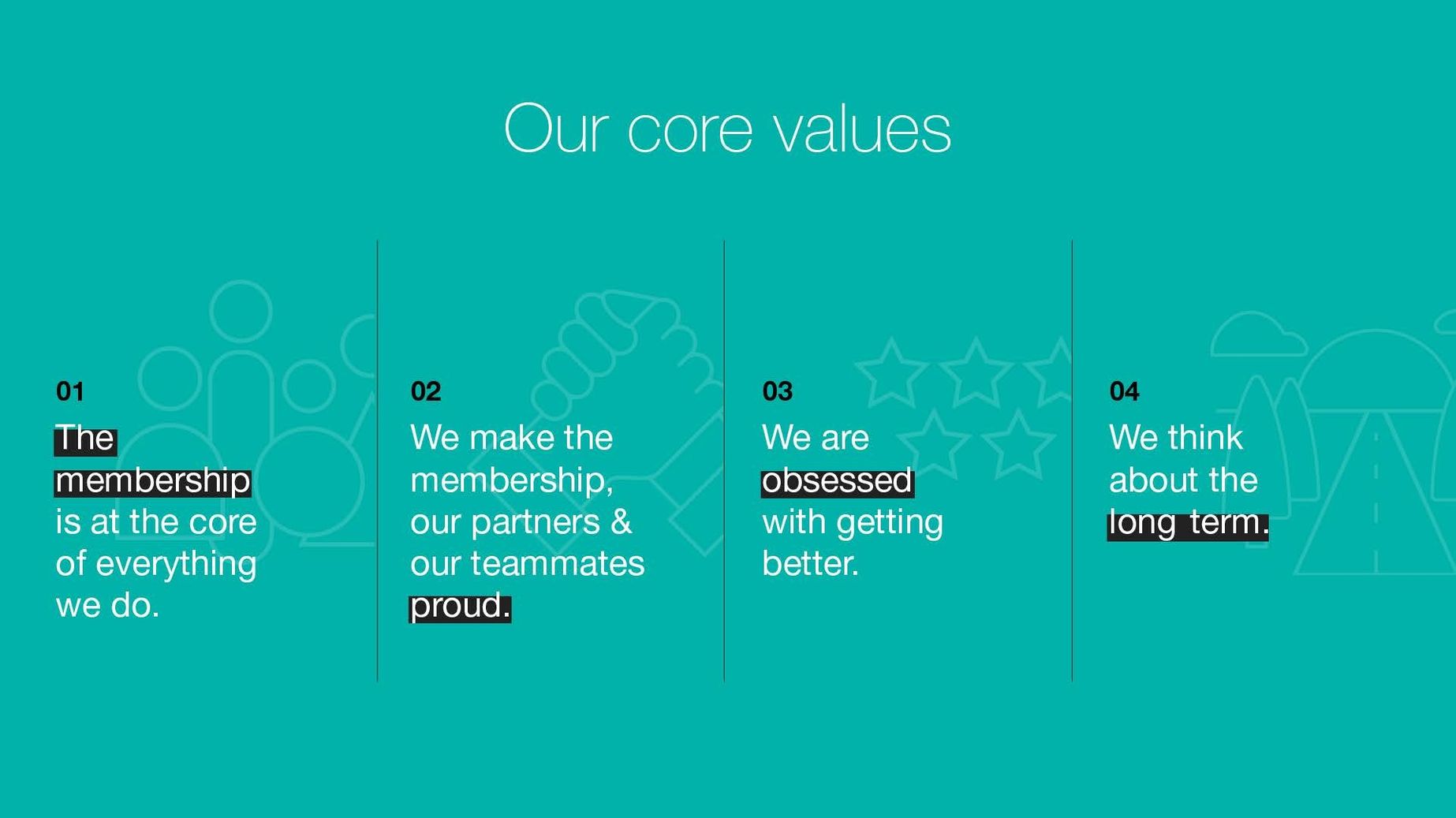

In addition to our commitments, our core values guide how we work together and aspire to do business every day.

Challenges remain, and we’re in this together

I feel strongly that I must continue to be transparent about the challenges we face and what we are doing to address them. A challenge unique to all insurance companies, PURE included, is that we do not know our actual cost of goods sold (i.e., loss costs) at the time a quote is issued and a policy sold.

There are multiple reasons why loss costs, and, in turn, insurance premiums, have soared industrywide in recent years: extreme weather, increased frequency and severity of liability claims, increased severity in preventable homeowner claims—mainly but not limited to water damage—inflation impacting home rebuild and auto repair costs and rising reinsurance costs. I could go on.

Thankfully, we are seeing relief in some of these areas, but extreme weather and more frequent and severe liability claims show no signs of letting up, so we need to think creatively about how we might overcome these together.

2024 Extreme Weather at a Glance1

Insured losses from natural catastrophes totaled $117 billion. That is up 27% above the recent five-year average and 52% above the recent 10-year average.

Severe Convective Storms (SCS) accounted for nearly 50% of U.S. catastrophe losses. Within that category, hail caused more than half of the reported losses.

Average annual loss costs from SCS over the past five years are 425% higher than the same annual average loss experienced in the first decade of this century.

Five hurricanes made landfall in the U.S. We have now seen a major hurricane landfall in each year for the past five years. The last time this same trend appeared was between 1915 and 1919.

Canada experienced an all-time high for weather-related losses.

It certainly wasn’t a year for the faint of heart. So what now? As we see it, the best option is to double down on loss prevention and mitigation. But in order to succeed, this will take the collective effort of us all. If everyone does their part, we can bring loss costs and, in turn, premiums down while ensuring you have adequate coverage and peace of mind.

Casualty Environment

Claims costs for liability cases have been rising steadily for the past decade. Industry data from 2014 to 2023 shows an average annual severity increase of 9.4%,2 well above economic inflation over the same period. Excess liability claims data for PURE shows a similar trend in recent years. Analysis conducted by Assured Research, LLC, concluded that the collective 2023 combined ratio for 20 predominantly personal umbrella writers was 146%.3 Said another way, for every $1 of umbrella premium they wrote, they paid $1.46 in losses and expenses.

This is simply unsustainable. There are many reasons for higher severities, including higher medical costs, a more aggressive plaintiffs’ bar, and changes in juror sentiments towards defendants, amongst others. We will continue to work with our industry-focused advocacy groups like the National Association of Mutual Insurance Companies (NAMIC) to push for regulatory reforms where they are needed the most, but having adequate excess liability limits is one of the most important considerations you should have, especially in a heightened loss-severity period such as in today’s casualty environment.

Staying connected

As always, we will continue to analyze risk and the claims impacting the membership and will continue to share advice and offer solutions to help better protect you. In addition to the advice you will read in the report, we now share a quarterly newsletter giving us another platform to share advice, updates and progress. I hope you will read the next issue when it hits your email inbox.

As always, I greatly appreciate your membership, your trust and the proactive steps you have already taken to help mitigate or even prevent claims. I would be remiss if I did not also thank the 1,100 employees who come to work each day dedicated to delivering exceptional service; your brokers who act as your impartial advocate and who trust us enough to recommend us to you; and finally, the members of the Subscribers’ Advisory Committee (SAC) for all of the work they do in making the voice of the membership heard.

Wishing you all the best for 2025 and beyond,

Martin Leitch

Chief Executive Officer

1. Gallagher Re, Natural Catastrophe and Climate Report: 2024, January 2025. 2. Guy Carpenter, Casualty Market Update—U.S. Insurers Adapting to Evolving Markets, October 2024. (Note that the excess liability data in this report combines both commercial and personal lines.) 3. Assured Research, LLC, Assured Briefing, August 2024.